In the volatile and unpredictable world of financial markets, risk management is not just a necessity—it’s an art. One of the most effective tools investors use for managing risk and navigating the turbulent waters of the markets is options hedging. Employing strategic options positions can provide a safety net for your portfolio, mitigating potential losses and helping you maintain steady financial growth, even amidst market uncertainties. What are the best options hedging strategies?

In this blog post, we will explore the realm of options hedging strategies, delving deep into their mechanisms, applications, and the potential benefits they can offer to both individual and institutional investors. Our journey will take us through an array of concepts, from basic put and call options, to more complex strategies like straddles, strangles, and collars.

Whether you’re a seasoned trader wanting to diversify your risk management toolbox, or a beginner looking to understand the fundamentals, this comprehensive guide will provide you with a solid foundation and a practical understanding of options hedging strategies.

From protective puts to iron condors, these strategic maneuvers in the options market are like chess moves in the game of investing. They can help you safeguard your assets, capitalize on market volatility, and gain the upper hand in your investing journey. So, strap in as we demystify the world of options hedging, and learn how these strategies can play a pivotal role in your financial portfolio.

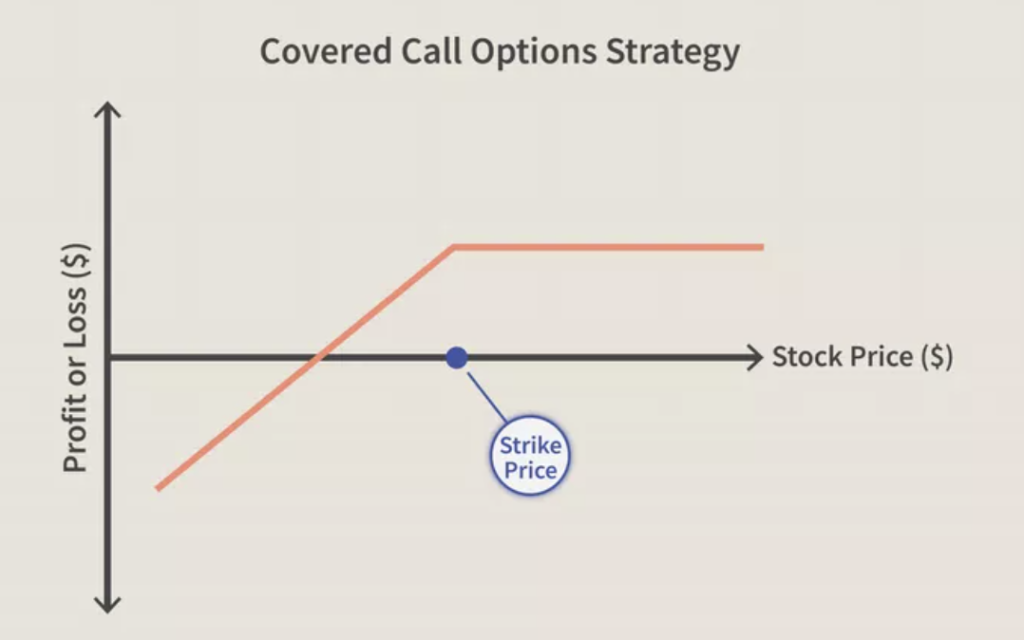

1. Covered Calls

Covered calls are a type of options trading strategy that can be used to generate income and provide a limited amount of downside protection. The strategy involves owning the underlying asset and selling call options against that asset. The term “covered” comes from the fact that the underlying assets are owned and can be delivered if the options are exercised.

Here’s how it works:

- Own the Underlying Asset: First, you need to own the underlying asset (typically stocks). For example, let’s say you own 100 shares of XYZ Corporation, which is currently trading at $50 per share.

- Sell a Call Option: Next, you sell (or “write”) a call option for the shares you own. The call option gives the buyer the right, but not the obligation, to buy your shares at a specified price (the “strike price”) within a certain period (until the “expiration date”). For instance, you might sell a call option with a strike price of $55 that expires in one month. You receive a premium (the price of the option) for selling this option.

The outcome depends on the price movement of the underlying stock:

- If the stock price stays below $55 (the strike price), the option will not be exercised by the buyer (as they won’t buy the stock for $55 when it’s available for less on the open market). You keep the premium from selling the option, and you still own your shares, which you can continue to hold or sell.

- If the stock price rises above $55, the option will likely be exercised. You must sell your shares for $55 each (even if the market price is higher). However, you keep the premium and make a $5 profit per share (the difference between the strike price and the price at which you bought the shares).

While covered calls can provide income from the premiums and offer a bit of downside protection (as the premium can offset minor drops in the underlying stock’s price), there are risks involved:

- Limited Upside: If the stock price rises significantly, you miss out on the potential profits because you’re obligated to sell your shares at the strike price.

- Downside Risk: If the stock’s price falls significantly, the premium you received provides only limited protection. For example, if the stock price drops to $40, you’d still lose $10 per share, even after accounting for the premium.

Remember, writing covered calls is a moderately complex strategy that requires a thorough understanding of options and their associated risks. Always make sure you understand the strategy and its potential outcomes before using it. One of the best options hedging strategies!

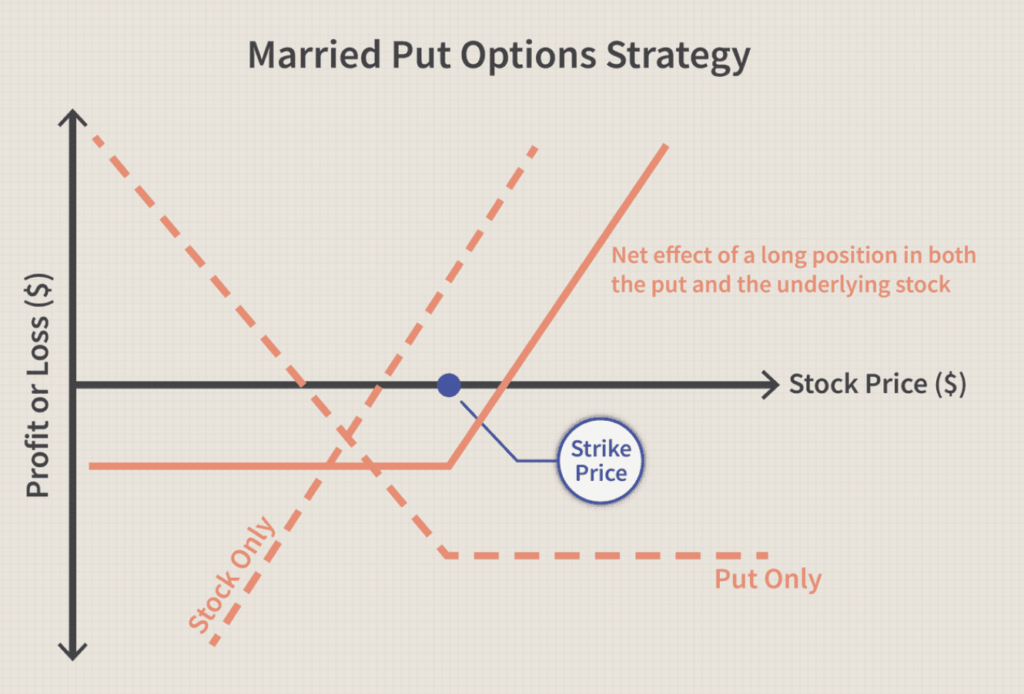

2. Protective Puts

A protective put is another popular options hedging strategy, often used to protect against a potential drop in the price of an underlying asset. It is also commonly known as a “put hedge” or “portfolio insurance”. In this strategy, an investor who owns shares of a stock purchases put options for the same stock to guard against a decline in the stock’s price.

Here’s how it works:

- Own the Underlying Asset: Similar to a covered call, you first need to own the underlying asset. For instance, you own 100 shares of XYZ Corporation, currently trading at $50 per share.

- Buy a Put Option: You then buy a put option for the same shares. A put option gives you the right, but not the obligation, to sell your shares at a specified price (the “strike price”) within a certain period (until the “expiration date”). For example, you might buy a put option with a strike price of $45 that expires in one month. This put option will cost you a premium (the price of the option).

Here are the possible outcomes:

- If the stock price falls below $45 (the strike price), you can exercise the option and sell your shares for $45 each, limiting your losses. The amount you lose is offset by the strike price, although you’ve paid a premium for the put option.

- If the stock price remains above $45, the put option will expire worthless. However, you still own your shares and can continue to hold or sell them. The only loss in this scenario is the premium you paid for the put option.

The protective put strategy provides a safety net against a significant drop in stock price. However, it comes with its costs and risks:

- Cost of the Put Option: The put option comes with a premium that you have to pay upfront, which can reduce your overall investment return.

- Limited Protection: The protection is limited to the strike price of the put option. If the stock price falls significantly below the strike price, you still incur a loss (though less than if you didn’t have the put).

Like any investment strategy, a protective put requires a clear understanding of options and the associated risks. Be sure to fully understand these before implementing such a strategy.

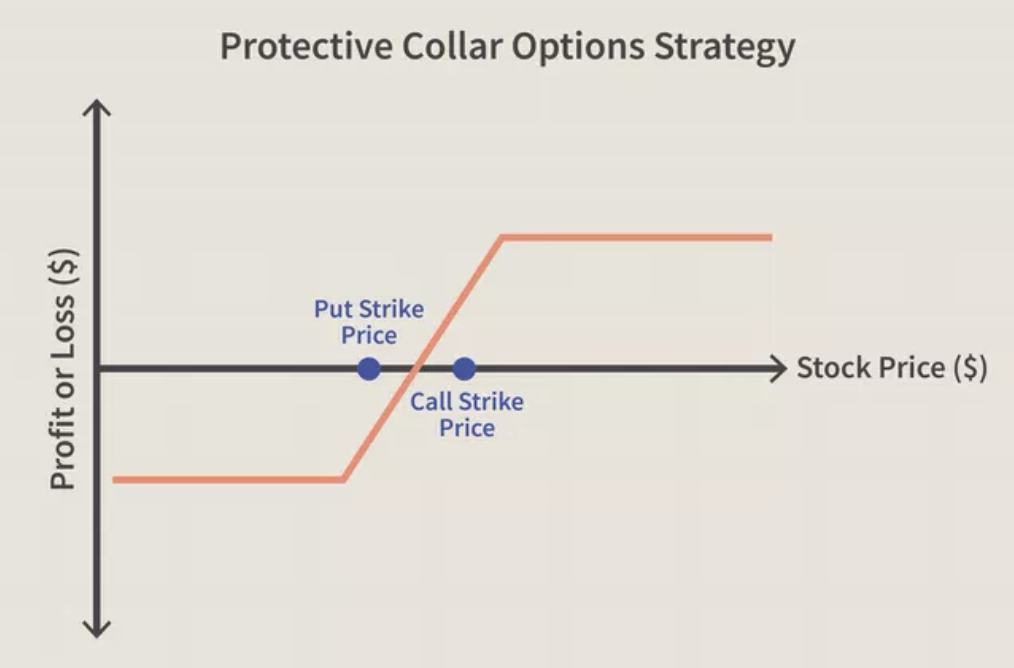

3. Collar Strategy

A collar strategy, also known as a hedge wrapper, is an options strategy that is designed to limit the risk associated with large price swings in the underlying asset by establishing a ‘range’ in which the price can fluctuate. It is typically used when an investor wants to limit their exposure to volatility and is willing to give up some potential gain to do so.

The collar strategy is executed by owning the underlying asset, while simultaneously buying protective puts and writing covered calls on that same asset. The premiums from the written calls can offset the cost of buying the puts.

Here’s how it works:

- Own the Underlying Asset: Similar to the strategies above, the first step is to own the underlying asset. For example, you own 100 shares of XYZ Corporation, currently trading at $50 per share.

- Buy a Put Option: You buy a put option, which gives you the right to sell your shares at a specific price (the “strike price”) until a certain date. This protects you from a significant decrease in the stock’s price. For example, you might buy a put option with a strike price of $45 that expires in a month. You pay a premium for this option.

- Write a Call Option: At the same time, you write a call option for the same shares. This means someone pays you a premium for the right to buy your shares at a certain price until a certain date. You might write a call option with a strike price of $55. The premium you receive for the call option can offset the cost of buying the put option.

Now, depending on the stock price:

- If the stock price falls below $45, you can exercise your put option and limit your losses.

- If the stock price rises above $55, your shares will likely be bought (called away) at $55.

- If the stock price stays between $45 and $55, both options expire worthless, but you still own your shares.

So, a collar strategy caps both the potential upside and downside of an investment. The cost of the puts is offset by the income from the calls, making it a cost-effective strategy for limiting risk if you’re worried about short-term volatility in your stock position.

As always, this strategy requires a clear understanding of options and their associated risks. You should only implement this strategy if you fully understand these aspects and are comfortable with them. One of the best options hedging strategies!

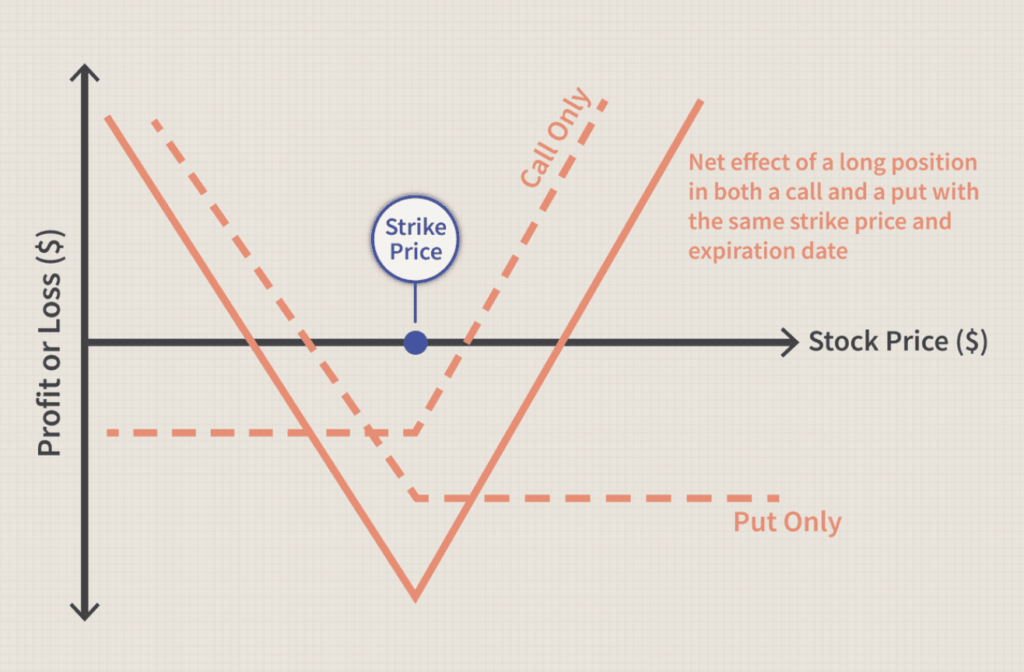

4. Long Straddle

A long straddle is an options strategy that allows an investor to profit when the underlying asset makes a significant move, regardless of the direction. The long straddle is not primarily a hedging strategy; it’s more of a speculative or directional strategy that is betting on volatility. It involves buying a call option and a put option with the same strike price and expiration date.

Here’s how it works:

- Identify the Underlying Asset: First, identify the underlying asset. For example, let’s say the asset is stock XYZ, currently trading at $50 per share.

- Buy a Call Option: You buy a call option for XYZ with a strike price of $50 that expires in one month. This gives you the right, but not the obligation, to buy XYZ at $50 at any time before the option expires. You pay a premium for this option.

- Buy a Put Option: Simultaneously, you buy a put option for XYZ with the same strike price and expiration date. This gives you the right to sell XYZ at $50 before the option expires. You also pay a premium for this option.

The long straddle strategy profits when the price of the underlying asset makes a significant move either up or down. Here are the potential scenarios:

- If the price of XYZ moves up to $60, the call option becomes valuable, while the put option expires worthless. Your profit would be the increase in the stock price minus the premiums paid for the options.

- If the price of XYZ drops to $40, the put option becomes valuable, while the call option expires worthless. Your profit would be the decrease in the stock price from the strike price, minus the premiums paid.

- If the price of XYZ remains close to $50 and doesn’t move much, both the call and put options will expire worthless. You would lose the premiums paid for both options, which is the maximum potential loss.

The long straddle strategy essentially bets on volatility. It is a high-risk, high-reward strategy that can result in significant profits if the price of the underlying asset makes a large move, but can also lead to significant losses if the price doesn’t move much.

As always, understanding the potential risks and rewards is crucial before implementing this or any other options strategy. Please consult with a financial advisor or do thorough research before executing such trades.