In the Modern Portfolio Theory (MPT), volatility is risk. That’s why, in this article, we have a look at volatility computations for crypto portfolios in Python.

If you want to control your risk as a trader, you need to up your game in terms of understanding of volatility.

Volatility can be calculated in different ways… but in this article we will do it using standard deviation on historical data.

We define various portfolios of crypto assets and compute their standard deviation across a year: the annualized volatility.

Based on the results, what is the less risky crypto portfolio?

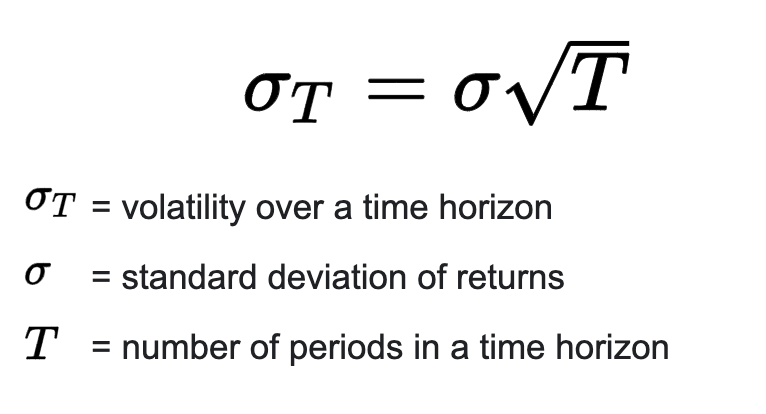

1. What Is The Annualized Volatility?

The annualized volatility of a portfolio is the volatility over a given year. The general volatility formula for any period and time horizons is:

In the formula above: T is equal to 365, the number of trading days in a year as crypto markets are trading every day.

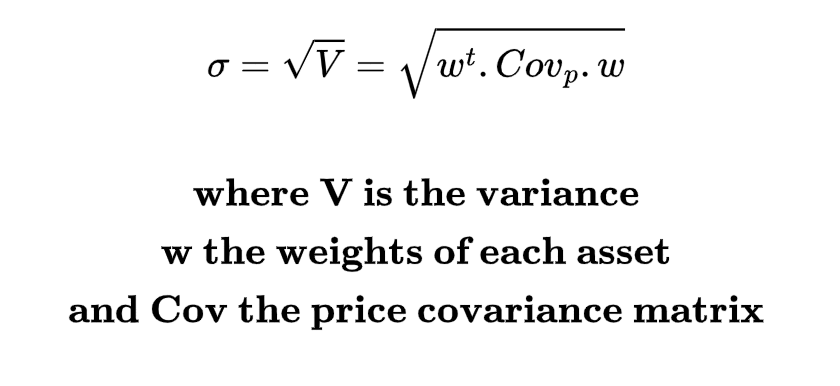

Now, how to get the standard deviation of returns of a portfolio based on the weight of each asset?

Using the price covariance and the weight vector (weight for each asset) in the portfolio:

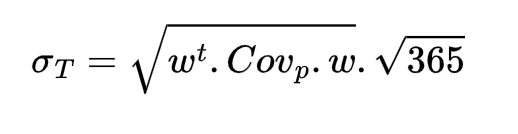

So the annualized volatility (T=365 days) is:

2. Get The Price Data

Let’s imagine you have a balanced portfolio Bitcoin, Cardano, Polkadot, Ethereum:

w = [0.25, 0.25, 0.25, 0.25]We get the prices daily over a period of one year

You can download them from yahoo finance and load them with a simple snippet:

import pandas as pd

files = ["BTC-USD.csv", "ADA-USD.csv", "DOT-USD.csv", "ETH-USD.csv"]

dfs = []

for file in files:

df = pd.read_csv(file).drop(columns=["Open", "High", "Low", "Adj Close", "Volume"])

df["Close"] = df["Close"].astype(float)

df = df.rename(columns={"Close": file.split("-")[0]})

dfs.append(df)

dfs = reduce(lambda df1,df2: pd.merge(df1,df2, on='Date'), dfs)

It gives you the prices by date in a dataframe:

Date BTC ADA DOT ETH

0 2021-12-17 46202.144531 1.219892 24.663027 3879.486572

1 2021-12-18 46848.777344 1.242534 25.490757 3960.860107

2 2021-12-19 46707.015625 1.244661 24.791401 3922.592529

3 2021-12-20 46880.277344 1.238240 24.050674 3933.844482

4 2021-12-21 48936.613281 1.280859 25.194195 4020.260010

.. ... ... ... ... ...

361 2022-12-13 17781.318359 0.312865 5.276955 1320.549194

362 2022-12-14 17815.650391 0.308134 5.215210 1309.328735

363 2022-12-15 17364.865234 0.300201 5.226642 1266.353882

364 2022-12-16 16647.484375 0.264070 4.655857 1168.259399

365 2022-12-17 16708.097656 0.263521 4.672759 1178.416260

3. Compute The Annualized Volatility

To calculate the annualised volatility, we simply apply the formula defined in (1) to the dataframe of prices defined in (2):

import numpy as np

weights = [0.25, 0.25, 0.25, 0.25]

portfolio_returns = dfs.pct_change()

covariance = returns.cov()

portfolio_variance = np.transpose(self.weights) @ covariance @ self.weights

annualized_volatility = np.sqrt(portfolio_variance) * sqrt(365)You’ll get the following annualized volatility: 0.781

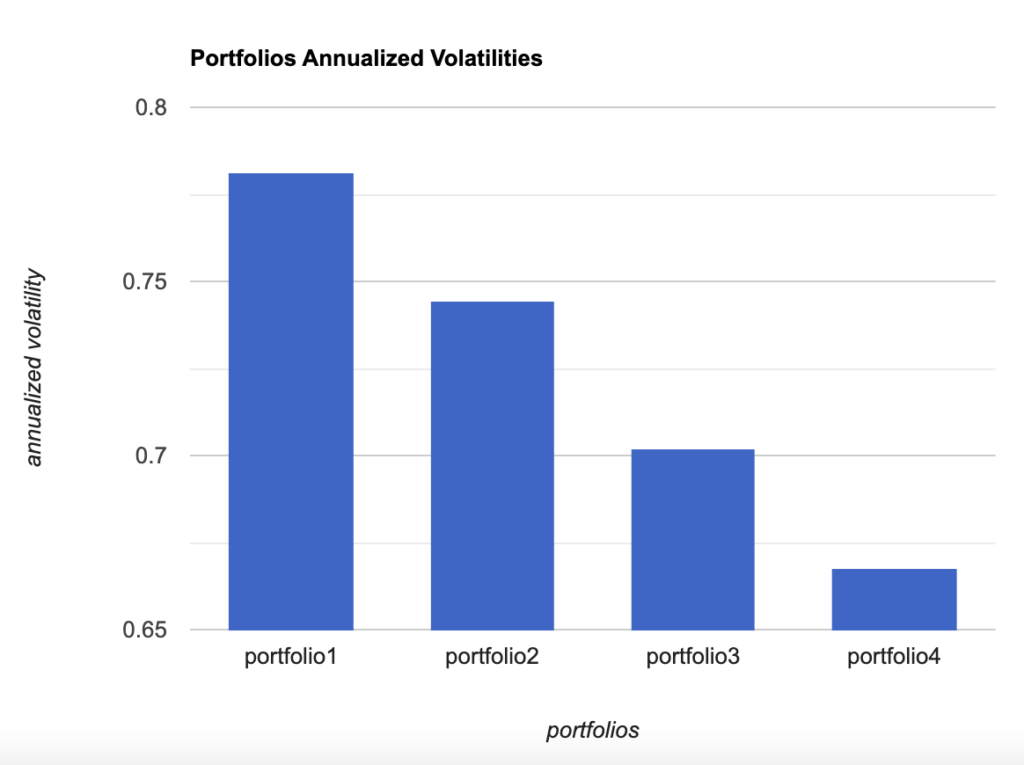

Now, let’s create 4 different portfolios with different weights on BTC, ADA, DOT and ETH:

weights_portfolio_1 = [0.25, 0.25, 0.25, 0.25]

weights_portfolio_2 = [0.4, 0.2, 0.2, 0.2]

weights_portfolio_3 = [0.6, 0.1, 0.1, 0.2]

weights_portfolio_4 = [0.8, 0.05, 0.05, 0.1]They give the following volatilities:

4. Conclusion

Surprise, surprise, the more Bitcoin you have in your portfolio, the lower the annualized volatility of your portfolio.

If you want to minimize risk at any cost, you know what to do: increase your exposure to Bitcoin.

The real question that will come in an upcoming article (that will probably look like our stocks machine learning model) is how to minimize the risk-adjusted-returns.

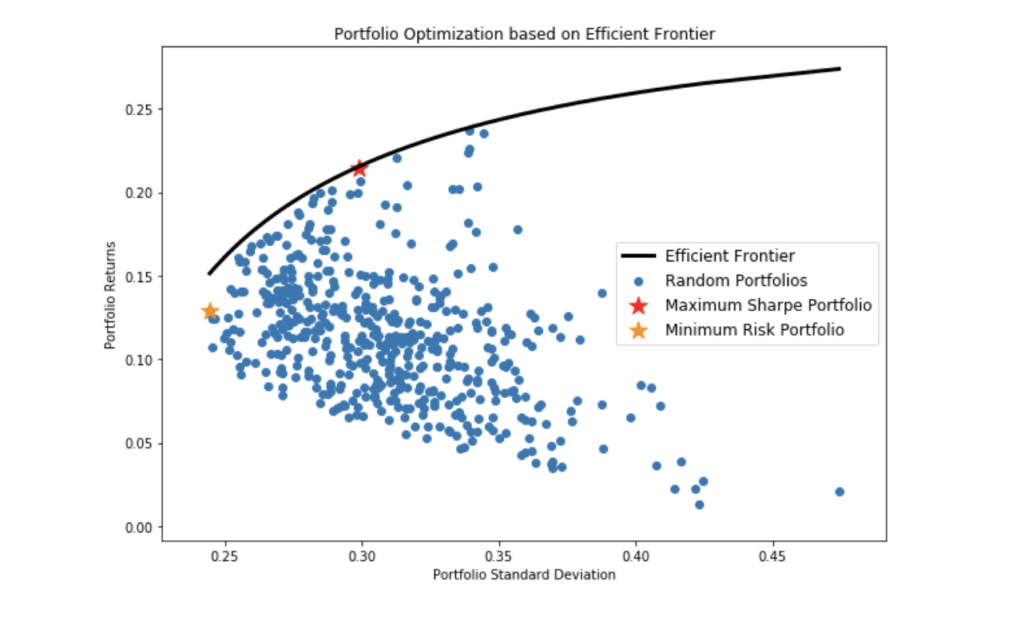

There is an optimal risk-return frontier that can be discovered by generating a myriad of virtual portfolios based on random assets weights via Montecarlo simulations (blue points):

How to find that black frontier? What does it mean to be on it? Where exactly should you be on it depending on your risk appetite? Stay tuned for more crypto volatility content in Python.

Thanks for reading.

n.b: this is not financial advice